Quick Links

Ghoomer Opens to Low First Day Collection at the Box Office

R Balki's sports drama Ghoomer starring Abhishek Bachchan and Saiyami Kher released in cinemas on…

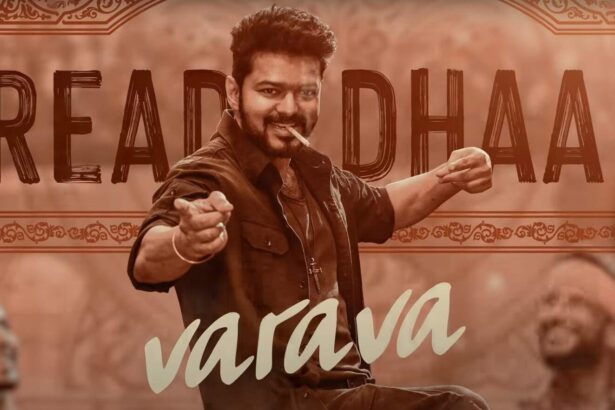

Vijay Faces Criticism Over Controversial Song Lyrics Amid Political Aspirations

Chennai: Fans have expressed disappointment and criticism towards actor Vijay, questioning his suitability for entering…

Aakhri Sach Episode 5 Release Date on Disney+ Hotstar, Story Predictions and Preview

Inspector Anya's high-stakes hunt to expose the truth behind the chilling ritualistic killings continues in…

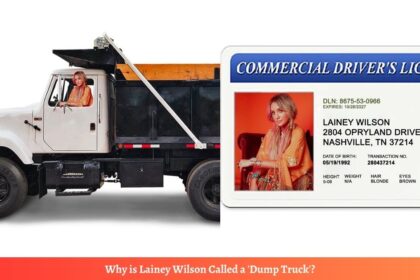

Why is Lainey Wilson Called a ‘Dump Truck’?

Lainey Wilson, the fast-rising country music singer and actress, has recently become known by an…

Is Cillian Murphy Played Any Role in the Dark Knight?

Cillian Murphy has emerged as one of the most compelling character actors of his generation,…

Who is TTF Vasan? Has TTF Vasan (Twin Throttlers) Died in a Bike Accident?

TTF Vasan, the wildly popular Tamil YouTube motovlogger renowned for his death-defying bike stunt videos…

Top 10 Most Daring Motovloggers in Tamil Nadu

Tamil Nadu's motovlogging scene is thriving, with talented content creators taking to two wheels to…

What Happened to Popular YouTuber TTF Vasan? Is he Alive?

Popular Tamil YouTube star TTF Vasan has been critically injured in a horrific bike accident…

Who is the No. 1 Motovlogger in Tamil Nadu?

Tamil Nadu has a thriving community of talented motovloggers. But one star stands out from…

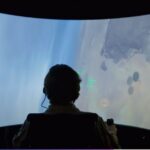

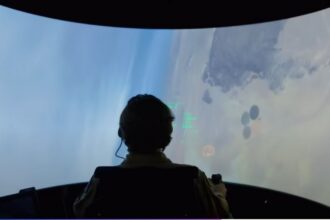

First AI vs Human Pilot Dogfight: Who Won the AIR Battle?

The US Air Force made history with the first-ever combat test between an AI-controlled aircraft and a human pilot. Conducted…

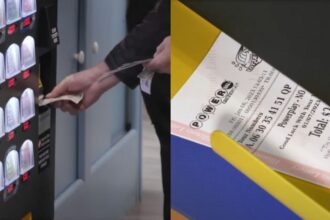

Here is Why Powerball Winning Numbers Trending in 2024

The year 2024 has seen an unprecedented level of public interest and social media engagement around Powerball winning numbers. With…

Created These Stunning Mother and Baby Unicorn AI Images with DALL-E 3

These breathtaking images were generated using the latest version of DALL-E 3.0, a cutting-edge AI image creation tool that has…

Anushka Sharma Returns Home: Son’s Privacy Prioritized

After a brief absence, Bollywood star Anushka Sharma has returned to India with her newborn son Akaay, making a notable…

A Diamond in the Rough: Finding Samurai in Aladdin?

Disney's animated classic "Aladdin" whisks us away to a vibrant tapestry of Arabian nights, filled with magic, adventure, and romance.…

21 Savage Accused of Scamming Adin Ross With Marked Cards

Rapper 21 Savage is facing backlash after being accused of cheating popular Twitch streamer Adin Ross with marked cards during…

Quaden Bayles Controversy on Bullying Scam: Know the Story

In February 2020, a heartbreaking video of 9-year-old Quaden Bayles went viral globally, bringing attention to the devastating impacts of…